What do Walmart, Amadeus and the NYT have in common?

It's not true that only digital-born companies will survive: there are indeed examples of established companies that have been adapted to this new world.

by Belén Romana

Disruption, a word on the verge of becoming as overused as digitization. We have come to a point where it is almost impossible for any business person to have a debate without these words entering the conversation. And usually these words come with an implicit conclusion: only digital-born companies will survive. Time, capital markets and customer expectations run against the so called “traditional companies”. And yet, there are indeed examples of established companies that have been able to find ways to adapt to this new world and remain appealing to their customers.

This is the story of some of those successes.

The Incredible Shrinking Time

The wave of change in technologies and markets is washing away a number of companies at a very fast pace. Boards are trying to cope with that pace with a wide range of instruments: from large IT investments to fierce M&A activity or changes in management, whilst at the same time redefining industry scope and boundaries.

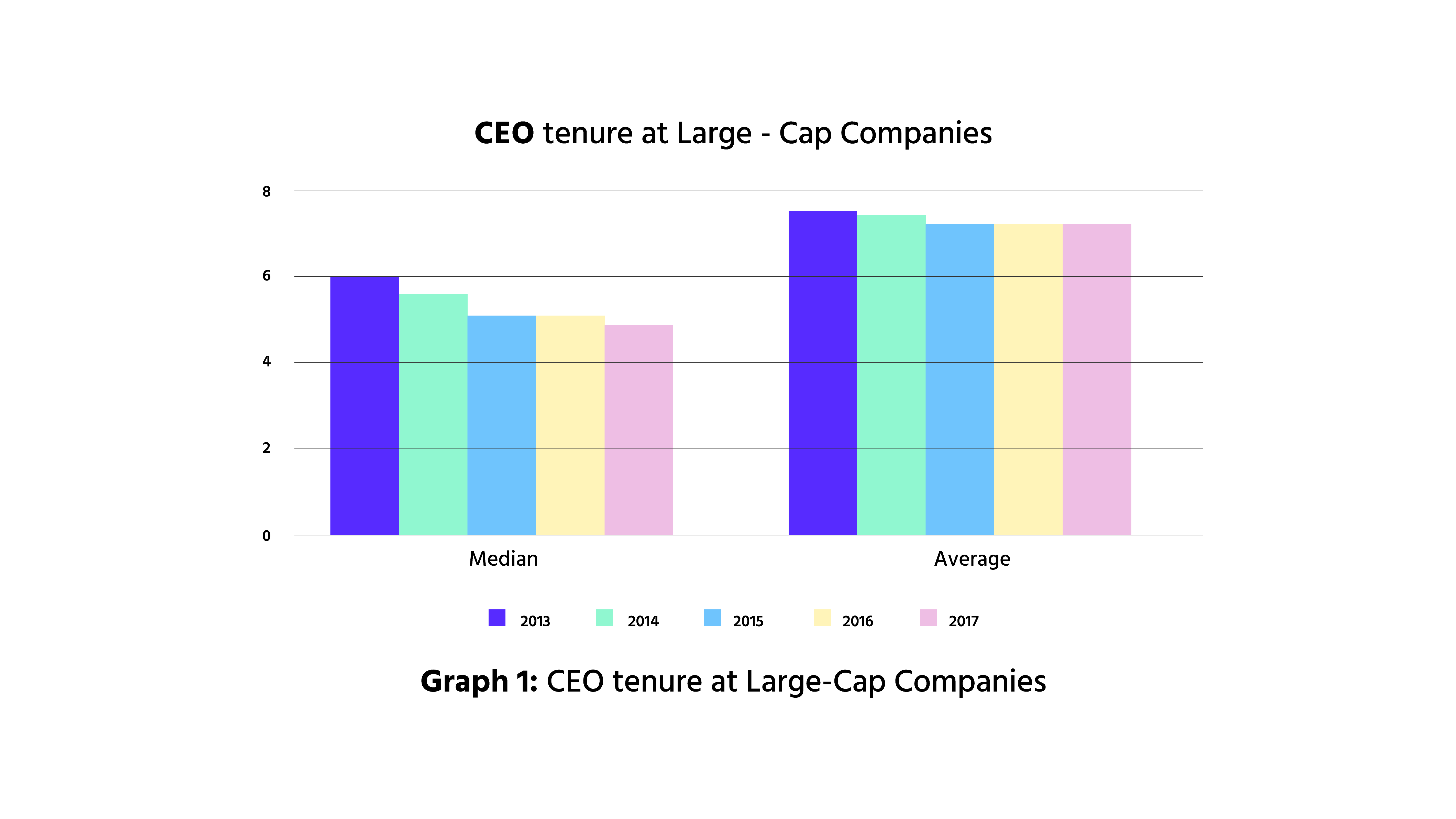

According to Dan Marcec (Director of Content & Communications at Equilar, Inc.), a recent Equilar study has shown that at large-cap S&P companies, CEOs´ median tenure has dropped a full year since 2013, down to 5 years (see graph 1).

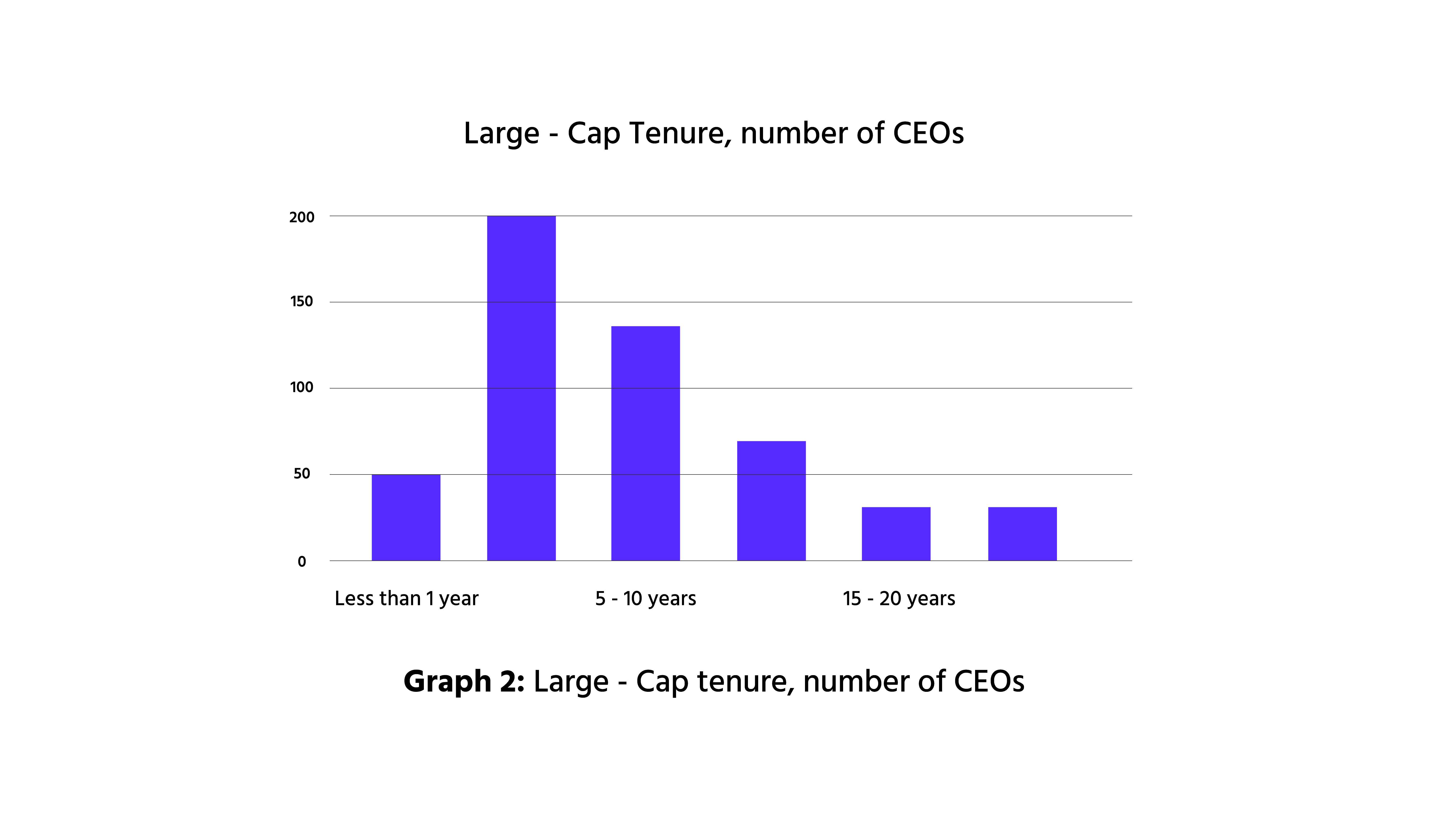

Consequently, by the end of 2017, more than a third of the CEOs had been in that position for less than 5 years (see graph 2).

Increasing pressure is exerted on large companies around the world. According to Pierre Nanterme, CEO of Accenture “Digital is the main reason just over half of the companies on the Fortune 500 have disappeared since the year 2000”.

The combined effects of a large number of technologies (from Big Data to Machine Learning) and trends (like customer centricity) have given birth to the so-called network effects, or “the winner takes it all”. The virtual circle of users, data, value and revenues has led to an increasing concentration in several markets, as well as a trend of “blurred lines” between sectors.

There are different strategies to cope with the changes imposed by the tech wave, all of them one way or the other encompassed in the term “digital transformation”. But the challenges are common to many industries: the need to manage time (especially for listed companies), the evolution of valuation or the stock price, the network effects and the accelerated and seemingly endless disruption. Incumbents were challenged by fast growing newcomers they did not even had under their radar.

In our view, Walmart, Amadeus and the New York Times have successfully navigated the huge changes their industries and markets have experienced over the past years. Each has followed a different strategy, but all of them have shown courage, leadership, out-of-the-box thinking and adaptability.

Walmart

Retail is undoubtedly in turmoil; Amazon has been able to expand its reach from books to cloud services and is now (again) changing consumers behavior through Alexa, the virtual assistant that has entered homes and, shortly, cars too.

The turmoil is huge and the pace is fast. It is hence key to manage time.

Of the 10 biggest retailers in 1990, only two remained in 2016. While it took Amazon, founded in 1994, only 22 years to reach revenue of $120 billion, being the fastest growing retailer. Walmart — born in 1962— needed 35 years to reach $100 billion.

Historically retail evolved and developed new concepts, from mom & pop stores, to department stores and malls, to answer new demographics and consumer needs. Amazon’s explosive growth is based on a technological change.

Walmart, who reigned in the universe of US retail with 12000 stores in 28 countries and more sales than any other company, is fiercely engaging in M&A to cope. In August 2016, it acquired Jet.com for $3,3 billion. Moosejaw (outdoor recreation apparel), Bonobos (men’s fashion basics), Eloquii (plus size clothing) and intimate apparel e-retailer Bare Necessities followed. At the time the transaction of Jet looked extremely expensive; yet it was probably the first step in ensuring Walmart’s survival.

However, the stock market has been merciless with Walmart and generous with Amazon.

As of April 2017, Amazon´s market capitalization equaled WalMart, Target, Macy´s Kroger, Nordstrom, Tiffany, Coach, William Sonoma, Tesco, Carrefour, Ikea and The Gap combined, as featured in “The Four” by professor Scott Galloway.

Last September, Amazon became the second $1 trillion company in US market. Compared to the total market, it is worth more than P&G, Coca Cola, and Pepsico combined.

This re-shaper of the retail industry could raise $2.1 billion before even breaking even. Professor Rita Gunther McGrath describes it as the “imagination premium” that investors are willing to pay for the promise of growth.

In sharp contrast, there was no premium for Walmart. When they announced in Q1 2016 that was increasing capital expenditures to invest in technology, it lost $20 billion in one day followed by $31 billion value lost in Q1 2018 when they revealed that e-commerce sales had slowed. Fearless and with the support of its lead investor, Walmart continued its pace of acquisitions.

The next challenge for Walmart is about using data plus intelligence to create value beyond what Amazon is already providing: how do they turn customers´ data into a competitive advantage, creating a network effect of their own.

With machine learning being the next frontier of disruption, Alexa is already deciding for us and anticipating what we want. Walmart needs to go fast not to be left out of customers´ choices by Amazon further accelerating a winner takes it all scenario.

New technologies drive endless disruption, and demand businesses to be continuously testing new ideas and endless experimentation and failure. But a high failure rate can only be afforded by those building barriers to entry and with easy access to capital. The Walmart fight is not over but it is still a work in progress!

The New York Times

First published on September 18, 1851, The New York Times (NYT) stated: “We publish today the first issue of the New-York Daily Times, and we intend to issue it every morning (Sundays excepted) for infinite years to come”.

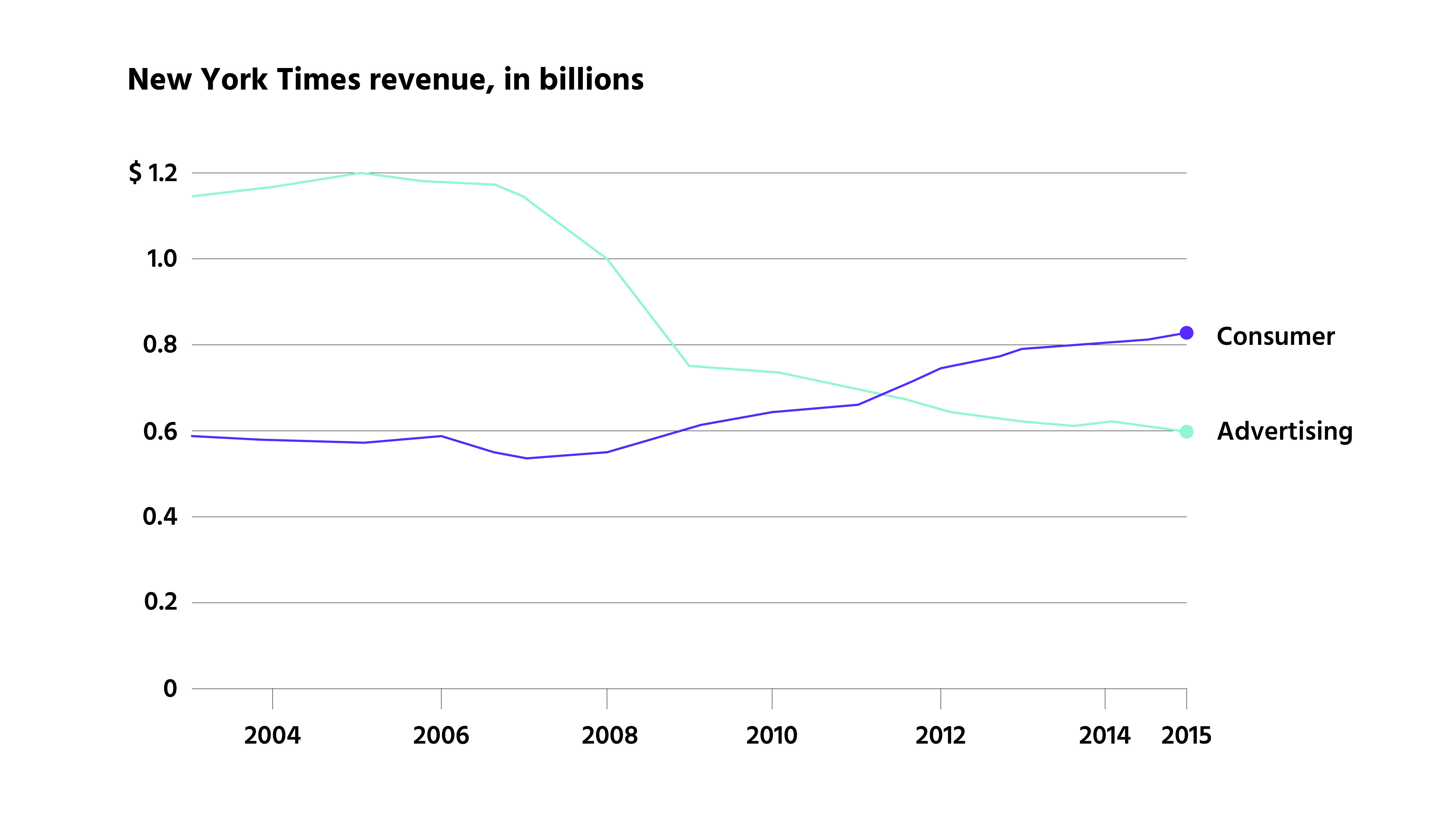

In its lifetime since then, it was a technological shift which forced NYT to review its business model. As a reaction to falling revenues from print advertising, they introduced a paywall to its website in 2011. After a slow start, in 2017 subscription revenue accounted for 60% of the company total revenue of $1,7 billion or $1,02 billion (see graph 3).

Graph 3: New York Times revenue, in billions

Could NYT have gained time by avoiding the distribution of valuable and precious content for free through Google and Facebook? Yes, they could have. It took them a while to realize; now they seem to be on the right track.

The NYT let Google handle their search function until they realized they were building a barrier to their readership data and contributing to the value of the search giant. On the other hand, being distributed by Facebook was, in terms of value creation, very valuable for the social network. Yet one could argue that it was damaging to society; as content from NYT was mixed with fake news, hence causing some of confusion we are witnessing today.

In short: free content was contributing to the growth of Google and Facebook while no value was added to the newspaper with a vocation of lasting infinite years.

Again, the stock price suffered. In 2005, NYT acquired About.com, an online provider of consumer information for $410 million. The acquisition was expected to have a double benefit: one, the purchasing of online know-how; but, more importantly, expecting that it would redefine how the market saw them, as there is a cost of looking like a traditional newspaper company instead of a digital one.

This last objective was not achieved as the price of their shares continued to fall, only picking up recently (see graph 4).

Graph 4: NYT, stock price history

The beauty of the subscription model, in spite of slow growth, is the access to data and the possibility to build intelligence around it. Maybe now it is the time to update its 1896 motto of “all the news that’s fit to print”.

Amadeus

The Amadeus IT Group, born in 1987, is a BtB company providing access to bookable content from airline companies, cruise liners, hotels and tour operators. It is an IT company that has been able to successfully face the revolution in travel. Today, more travel is sold over the internet than any other consumer product.

Founded by airlines (Air France, Iberia, Lufthansa and SAS) it has grown to a market cap over €30 billion and diversified into almost every way of travelling. In 2017, Amadeus controlled over 40% of the world travel reservations market and almost 30% of IT solutions for the travel industry worldwide.

Since the IPO in Spring 2010, the company’s EBITDA has grown 10% per annum, navigating the financial crisis as well as the changes both in the airline industry and in the way consumers buy travel. It has been through a succession of acquisitions that Amadeus has managed to adapt to the changing operational demands of its many clients, as well as spread its sectoral and geographical reach.

In the airline industry, it has widened its customer base to low-cost and hybrid segments (through the acquisition of Navitaire, an airline hosting firm provider of technology services to over 50 airline operators) and improved its service through Cytric, a global distribution system-agnostic platform acquired through one of their M&A moves.

This intense M&A activity has also been a key tool in expanding the hospitality sector, with the aim of offering a cloud-based suite of services that allows property owners to have a “single view of the guest” from a sales, management and customer perspective. Over the years, Amadeus bought Newmarket International (IT solutions for large and midsize hotel chains) and Itesso (a property management system provider), and also developed a strategic relationship with IHG to build a community-based Guest Reservation System.

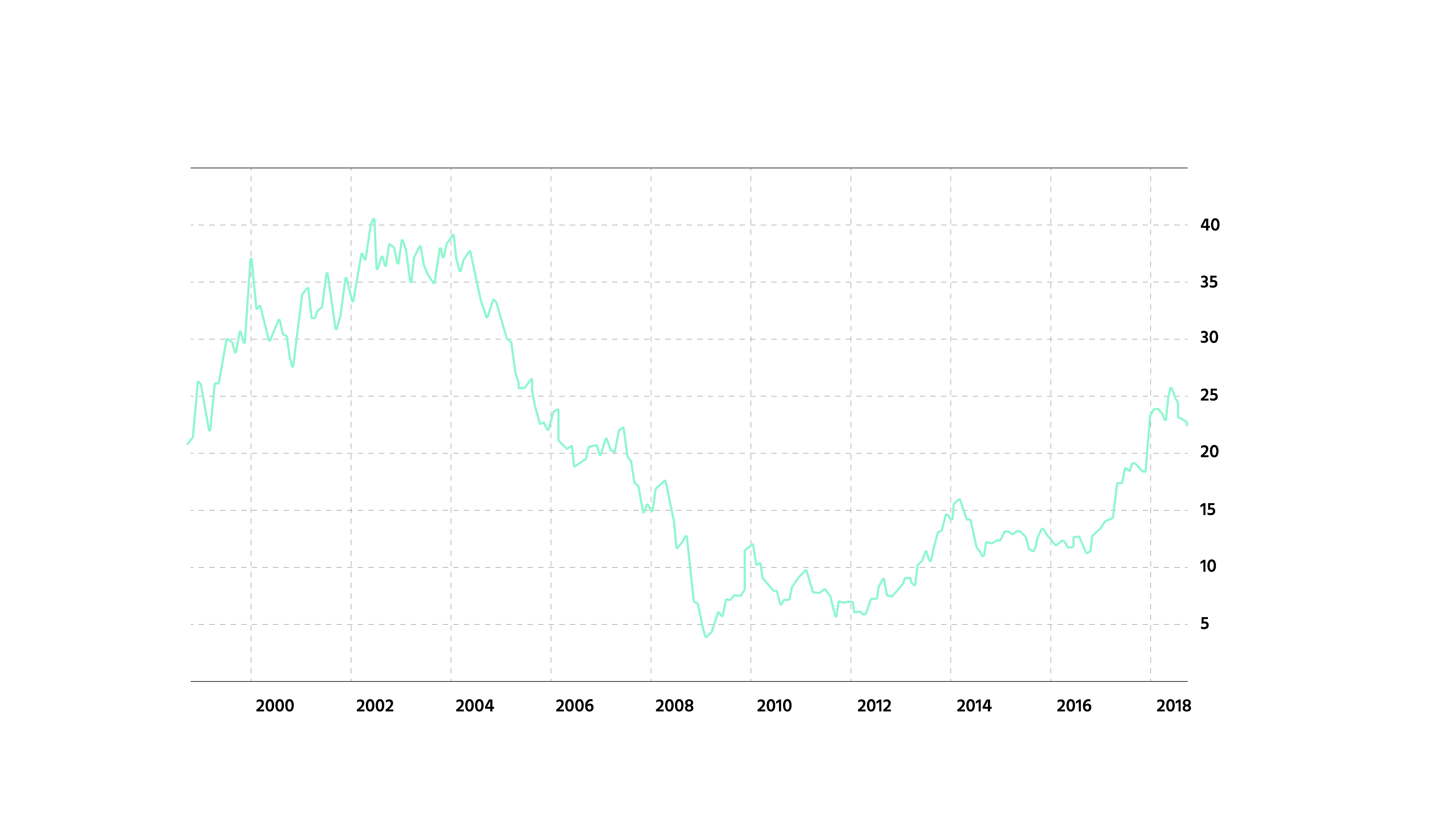

This constant and successful fight to keep at the forefront of its business has resulted in a continuous upward trend of Amadeus´s stock price, that has raised more than 600% in seven years. In terms of value, it is now worth more than the combination of its four founders.

But, as with many other companies, Amadeus had to cope with the stock markets short term demands. After an initial IPO in 1999, it was bought out by some private equity investors and one initial shareholder to help the company undertake the large investments and provide the time needed to cope with technological change. It took them 5 years to go back to the open market and become public again in Spring 2010 (see graph 5).

Graph 5: Amadeus, stock price history

But disruption is far from over: a combination of trends is impacting Amadeus´ business model. On the one hand, the airline consolidation has led to very few companies controlling regional markets (in the US, the top 40 airlines control 80% of the market — against 40% ten years ago; in Europe, the top 5 carriers control more than half of the market — versus 38% in 2007).

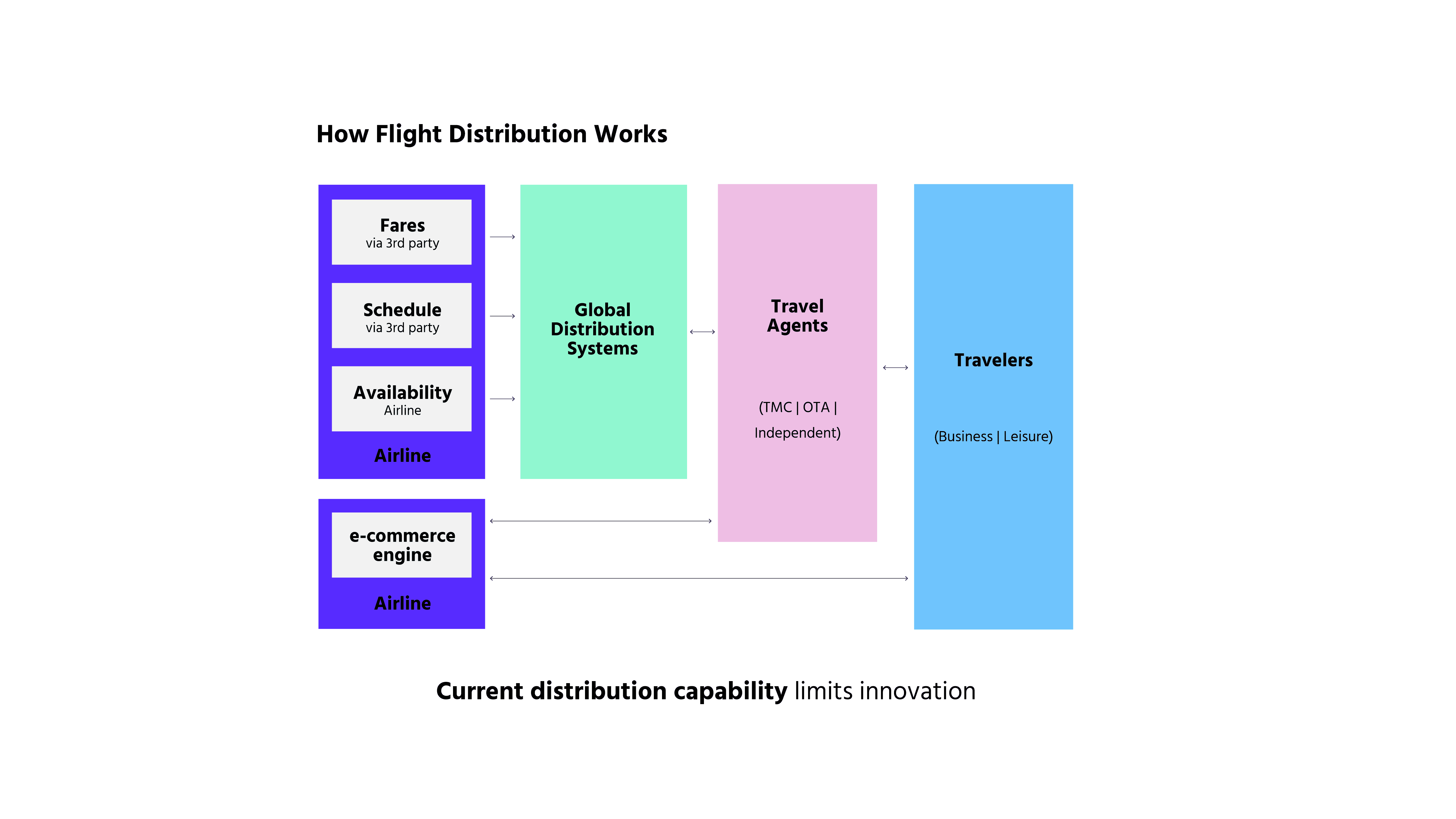

On the other hand, airlines are starting to grow increasingly interested in maximizing the value of their passengers, posing a threat to the Global Distribution System Amadeus has successfully mastered.

Chart 1: How Flight Distribution works

Therefore, Amadeus needs to keep on creating new lines of business and rewriting the way they develop their core activity. Hence, the company has been fostering new business lines such as Hospitality, Airports and Payments, while strengthening its role as an IT provider for Airline companies.

That is why Amadeus announced in early 2018 the acquisition of TravelClick — a hotel technology company that will allow them to start selling business intelligence software to large hotel chains as well as to mid-size and independent hotels (the bulk of the hospitality market) — for $1.5 billion.

What do these success stories have in common?

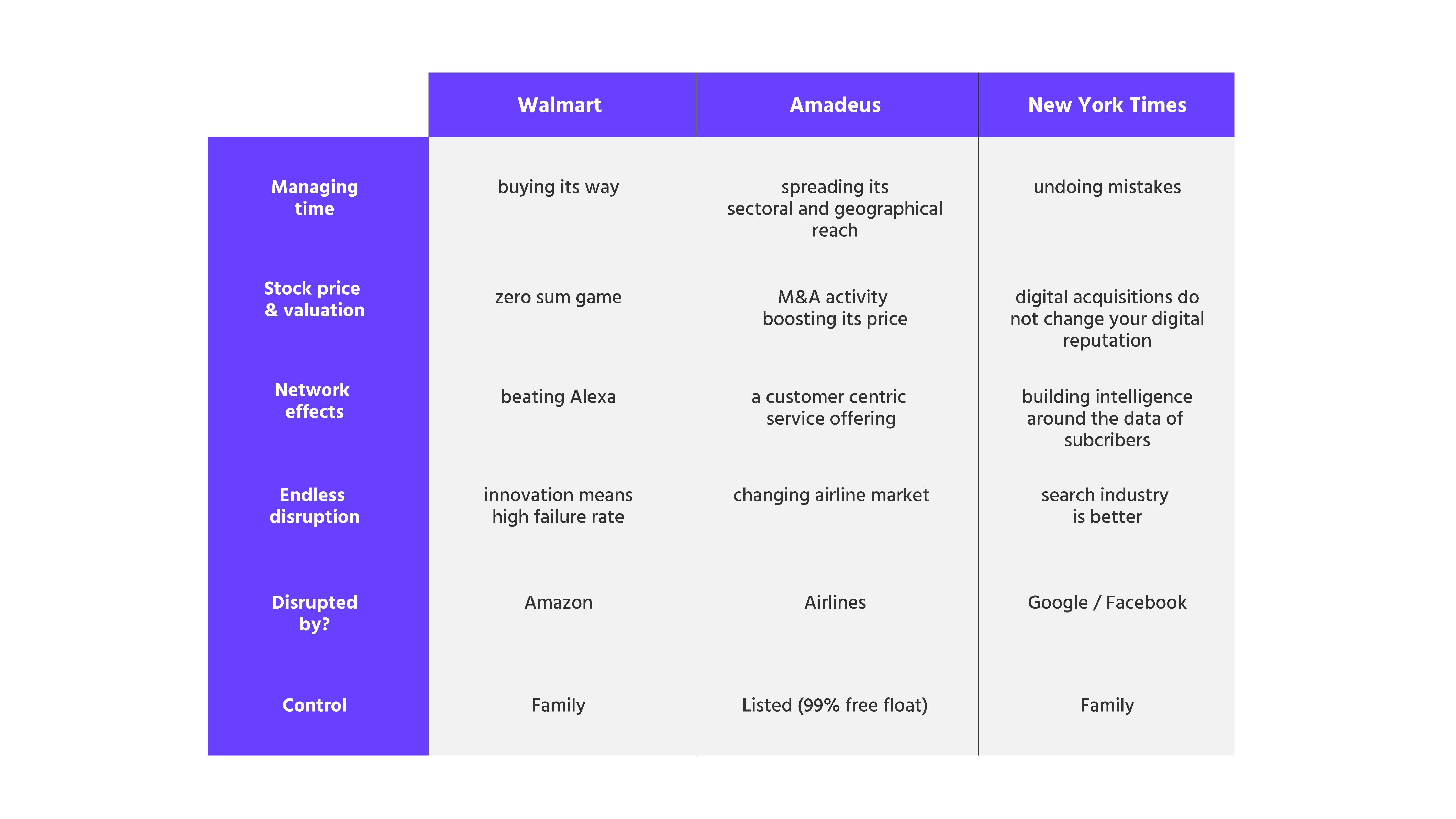

As said, the three companies have shown courage and determination in dealing with disruption, but that’s not the only common feature; there are others as well (see chart 2).

Chart 2: Walmart, Amadeus and NYT: common features

They all needed financial strength to cope with stock markets pressure. In two cases (Walmart and NYT) they are family owned businesses and the third one, after the first IPO, went through a buy back and only after material investments, a subsequent IPO. Hence, they all had the license to operate thanks to shareholders providing access to capital in funding their transformation.

Strong leadership has also been key to their success: the NYT had the same Chairman for twenty years (one member of the founder family), Amadeus had a long-term President and CEO coming from the company (he was Deputy CEO and responsible of Global Strategy back in 2009) and Walmart also had a Chairman from the founder family.

The three companies have embraced M&A as a way to acquire know how and technology, and in some cases to gain new customers and markets, widening their boundaries.

They all understood that technology was the driver of change and success, building the processes and business intelligence to own (and use) their customers data. That is an outstanding common feature: understanding who their end customer is and creating the products and services attuned to that customer.

Customer centricity is hence at the heart of their journey. A journey that is far from over as in the digital age, permanent change is the norm.